Fixed vs. Variable Interest Rates on Personal Loans: A Complete Guide

1. The Interest Rate Showdown

Choosing a loan is very important. It affects your financial future right away. The main choice is, between a fixed interest rate and a variable interest rate.

The Baseline Concept

Every personal loan has an interest rate. This rate helps figure out how much you have to pay for borrowing money.

Two Divergent Paths

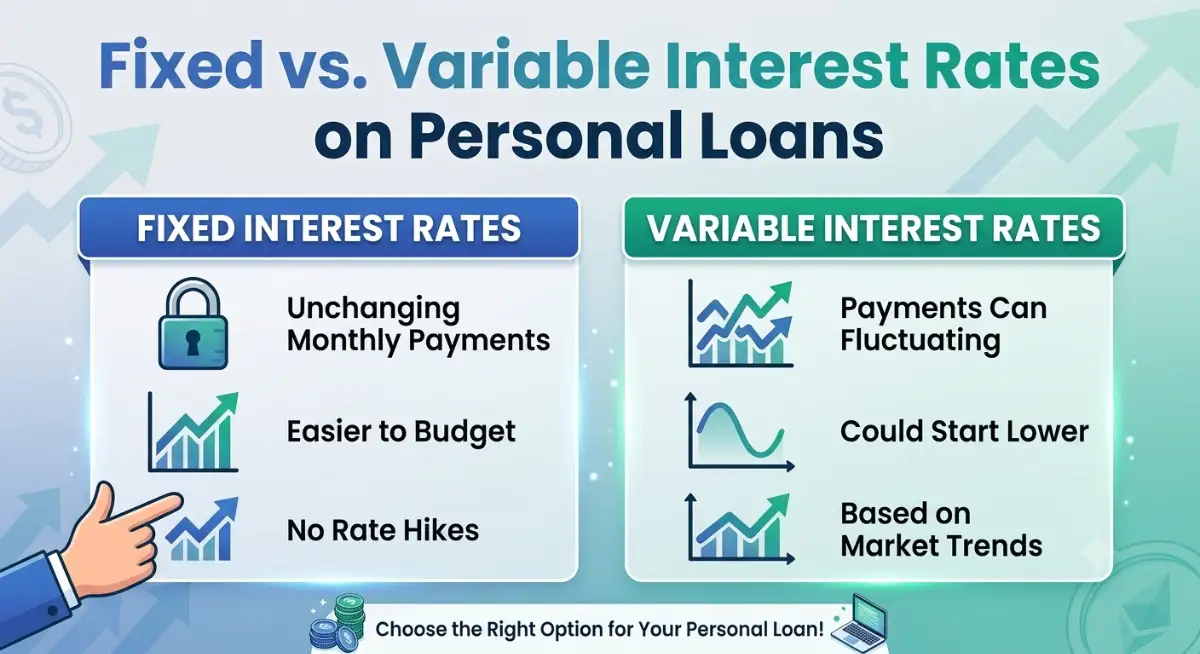

When you get a loan you have to choose between a fixed rate and a variable rate. A fixed rate stays the same while a variable rate can change with the market.

The Immediate Impact

Your choice will decide how much you pay each month the cost of your debt and how you plan your budget for a long time.

Strategic Decision Making

Picking the interest rate is crucial. It helps you save your money and manage your expenses better. A fixed interest rate gives you stability while a variable interest rate gives you flexibility. You have to choose what works best for you and your loan.

2. The Fixed Rate Fortress

Unyielding Stability For Your Budget

Fixed interest rates give you financial protection. You know what you will pay from day one until the loan ends.

- Locked Parameters: Your initial interest rate stays the same throughout the loan period. It does not change.

- Predictable Outflows: Your monthly payments are always the same. This makes it easy to plan your household budget. You do not have to worry about surprises.

- Market Insulation: Even if global financial markets are unstable or central banks increase interest rates your contract stays the same.

- Long-Term Peace: As a borrower you have clarity, on when your debt obligation ends. You know how much you have to pay and when you are done paying.

3. The Variable Rate Wave

Ride market trends to save money

Rates are like a financial plan that changes with the economy and the market.

- Fluid Financing: These interest rates go up and down following the changes in the market like the lending rate.

- Starting Bars: Variable options often start with lower interest rates than fixed rates.

- The Market Gamble: When the economy gets better and interest rates go down you will pay less each month.

- Risk Profile Awareness: People who borrow money need to be ready for interest rates to go up if the market changes so they need to have some money to handle it.

Variable rates can be good if you understand the risks, like the variable rate wave. You are ready for the changes in the market. The variable rate wave is about riding the market trends for maximum savings, with variable rates.

4. Head-to-Head Cost Analysis

Let us Break Down The Financial Math

We need to look at the financial math to see how each plan handles money over a long time.

- The Premium Pricing: When you choose a fixed option you usually pay a little more at the start. You get a guaranteed rate that will not change for a long time.

- The Discount Window: If you choose a package you might pay less at the start but this is only if the economy is doing well and you are willing to take some risks.

- Amortization Schedule Shifts: Fixed plans have a payment schedule that does not change but variable plans change with the market so the payments can go up or down.

- Total Expense Projections: To really know how much something will cost you need to balance the fixed expenses that you know about with the expenses that might change and this is not always easy to do with cost analysis of head-to-head cost analysis.

5. Winning With Fixed Rate Strategies

When To Choose The Secure Route

There are times when you really need to go with a fixed rate plan to manage your money wisely. This is true for people who have a budget and not a lot of extra money to spare.

- Tight Budget Frameworks: If you do not have a lot of money left over at the end of the month you should choose a fixed rate to avoid money problems.

- Extended Loan Terms: If you have a loan that you will be paying back for more than three years you should lock in your interest rate so you are protected from changes in the economy.

- Rising Rate Environments: When you hear that interest rates might be going up you should get a fixed rate soon as possible.

- Risk Averse Profiling: If you get worried when you think about what might happen to your money because of changes in the market you should choose a fixed rate so your payments are always the same.

6. Maximizing Variable Rate Advantages

Taking Advantage Of Changes In The Economy

Variable interest rates work well when the economy is changing and when it fits your personal schedule.

- Short Repayment Windows: If you want to pay off your debt in one year you can take advantage of the variable interest rates when you first get the loan.

- Falling Economic Indexes: When the economy is not doing well and banks are lowering interest rates variable rates can help you save money.

- Surplus Cash Cushioning: If you get a raise and your income goes up you can handle it when your payments go up sometimes.

- Prepayment Freedom Models: Variable rate loans often let you pay off the loan without having to pay a lot of extra fees.

7. The Ultimate Selection Matrix

Mapping Your Perfect Financial Match

To have money success for a time you need to make sure your personal loan structure fits with what you want to achieve in your life.

- Audit Personal Stability: You should really think about how stable your job is and how much money you get every month before you decide on a loan.

- Evaluate Loan Purpose: If you need money for an emergency you should get a loan with a fixed payment plan. If you need money to help you get through a big change you might want a loan with payments that can change.

- Project Market Directions: You should look at what smart people think will happen in the world to figure out what will happen to the market while you are paying back your loan.

- The Final Verdict: You should choose a loan with fixed payments if you want to be safe for a time. You can choose a loan with payments that can change if you want to save money quickly.

8. The Final Action Plan Checklist

Your Strategic Roadmap to Success

Before you sign any loan agreement use this checklist to make sure you are making a decision that is good for your long term financial security and the money you have now.

- Review Your Cash Flow Buffers: Look at your bank statements from the last six months to see if you can handle it if your monthly loan payments go up by 10 percent if you choose a variable rate loan.

- Assess How Long You Will Have The Loan: If it will take you more than 36 months to pay back the loan think about choosing a fixed rate loan so you do not have to worry about what might happen with the economy in the long term.

- Check What Is Happening In The Market: Take a few minutes to look at what the central bank is doing with interest rates to see if they are low right now or going up.

- Compare The Total Interest You Will Pay: Use a loan calculator on the internet to see how interest you will pay over the whole life of the loan for both fixed rate loans and variable rate loans.

- Verify If There Are Any Fees For Paying Off The Loan Early: Always read the fine print to see if you will have to pay a fee if you pay off the loan early because this will help you decide if a variable rate loan is really a good choice for you.

- Final Decision Confidence: If you think you will worry about your loan payments going up and down you should choose a fixed rate loan because being able to sleep at night is important for your health and loan agreements and the loan itself.